Financial Planning for 2026

Financial planning for 2026 is more critical than ever. The world has entered a phase where financial decisions can no longer be based on assumptions, generic advice, or outdated experiences.

Why Financial Planning for 2026 Is No Longer Optional

Before entering a new year, most of us naturally start planning different aspects of our lives, career goals, family decisions, lifestyle changes, or business growth.

Yet the reality is simple: none of these plans can be sustainable without a clear and realistic financial plan behind them.

Financial planning for 2026 is more critical than ever. The world has entered a phase where financial decisions can no longer be based on assumptions, generic advice, or outdated experiences. A credible financial plan today must:

- Be grounded in lessons learned from recent global events

- Reflect the real risks shaping the global economy

- Remain flexible across multiple future scenarios

Over the past year, the global economy has faced a wide range of risks from geopolitical tensions and political instability to inflationary pressures and market volatility. One of the clearest outcomes of this uncertainty was seen in the markets: gold prices reached historical highs after many years, highlighting the renewed role of safe-haven assets during periods of instability.

As a result, many investors now believe that gold and silver may continue to play an important role in financial planning and portfolio construction not as standalone solutions, but as tools for managing risk and preserving long-term value.

At the same time, political developments have become increasingly influential in shaping financial planning decisions for 2026. At the beginning of the new year, geopolitical conflicts including rising tensions and regime changes in countries such as Venezuela once again demonstrated how quickly political events can reshape markets, currencies, and capital flows. Meanwhile, ongoing instability in the Middle East continues to be a key source of uncertainty for global investment decisions.

All of these developments wars, political shifts, and market disruptions have a direct impact on investment outcomes, long-term financial decisions, and the way individuals and families should plan their wealth.

For this reason, entering 2026 without a clear financial plan exposes individuals and families to risks that are not only foreseeable, but often manageable with the right strategy.

At Dar al-Tharwa, we have developed a structured approach to financial planning for 2026 based on in-depth analysis conducted by our research and strategy team. This approach is grounded in our internal report, 2026 Economic & Financial Markets Outlook, which provides a data-driven and scenario-based view of the global economy and financial markets.

This article is not intended to offer generic financial tips or one-size-fits-all solutions. Instead, it is designed to serve as a reference framework for your personal financial planning in 2026.

Throughout this guide, you will:

- Understand the key global risks shaping financial markets in 2026

- Identify investment opportunities that emerge alongside these risks

- Learn how to design a balanced, forward-looking investment portfolio aligned with your personal financial situation and long-term goals

Financial success in 2026 will not come from avoiding risk entirely, but from understanding risks clearly and using opportunities wisely alongside them.

With informed planning and disciplined decision-making, 2026 can become a year where you strengthen financial stability and build a more secure future for yourself and your family.

Financial Planning Outlook for 2026

Financial Planning in a Year of Limited Growth and Persistent Risks

To build a reliable financial planning framework for 2026, it is essential to first understand where the global economy stands today. Based on macroeconomic analysis, the global economy, particularly the U.S. economy, which plays a decisive role in global financial markets has entered a phase that cannot be described as a boom, nor as a crisis.

Instead, 2026 represents a transitionary period. Economic activity continues, but at a slower pace, with higher sensitivity to risks and less room for error. Growth has not disappeared, but it has become more selective and fragile.

The key characteristics of economic growth in 2026 are clear:

- Economic growth remains positive

- But it is limited and fragile

- And highly sensitive to data releases, policy decisions, and external risks

This environment directly shapes how families and investors should approach financial planning in 2026, fundamentally changing decision-making compared to previous years.

Economic Growth: Positive, but Limited and Sensitive

Economic forecasts suggest that real economic growth in 2026 will stabilize near long-term potential growth.

In simple terms, the global economy has moved out of an overheated phase, but it has not entered a deep recession.

This means the economy is operating in a zone where:

- Growth capacity is constrained

- Activity continues, but without strong momentum

- Small shocks can trigger outsized market reactions

What Does an “Overheated Economy” Mean and Why Is It Over?

An overheated economy refers to a phase in the economic cycle where:

- Demand grows faster than the economy’s real productive capacity

- Inflation accelerates

- Wages rise rapidly

- Asset prices climb beyond their intrinsic or fundamental value

A clear example of this phase was seen during 2021–2022, when:

- Money was cheap

- Liquidity was abundant

- Market optimism was widespread

During that period, nearly all assets appreciated, often regardless of underlying fundamentals. Investment decisions were frequently driven by momentum rather than valuation or risk assessment.

By contrast, this environment no longer exists in 2026.

The economy has shifted into a more balanced but highly sensitive phase, where:

- Broad, market-wide gains are rare

- Weak assets are penalized more quickly

- And the quality of asset selection has become decisive.

What Limited Growth Means for Financial Planning

In an environment of limited growth:

- Investors should not expect “the entire market” to deliver strong returns

- Poor decisions become costly faster

- Assets without real economic backing are far more vulnerable

For personal and family financial planning, this implies:

- Financial plans should not be built on the assumption of broad market growth

- Focus must shift toward assets with real profitability, sustainable cash flows, or clear intrinsic value

This shift is central to effective financial planning for 2026.

Inflation: Contained, but Still a Key Factor

Inflation has moved lower compared to previous years, but it has not disappeared from financial decision-making. In particular, services inflation linked to housing, healthcare, education, and wages remains persistent.

This has two important implications for financial planning:

- Household purchasing power continues to face gradual pressure

- Financial plans that focus only on nominal returns, rather than real returns, risk being misleading.

The Hidden Risk of Cash in Financial Planning

Holding cash without a clear strategy represents one of the most overlooked risks in financial planning for 2026.

For example:

- Cash that comfortably covers rent or education expenses today

- May cover a much smaller portion of those same costs just a few years later

As a result:

- Liquidity should serve as a short-term flexibility tool

- Not as a permanent store of wealth.

Assets That Tend to Perform Better Against Inflation

Within a disciplined financial planning framework, assets that help preserve value during inflationary periods become more important:

- Gold and precious metals:

Typically act as protective assets during uncertainty, helping preserve purchasing power. - Income-generating real estate:

Properties where rental income can adjust with inflation provide stability. - Profitable equities:

Companies that can pass rising costs on to customers tend to perform more resiliently. - Real assets:

Such as energy, infrastructure, and certain commodities that often move in line with inflation.

In effective financial planning, not every asset should be chosen for growth.

A portion of the portfolio must be designed explicitly to preserve value.

Interest Rates: From Shock to Risk Management

After a period of aggressive interest-rate hikes, monetary policy has entered a data-dependent pause. While rates may decline modestly in 2026, they remain structurally higher than in the previous decade.

This environment sends three clear signals for financial planning:

- Financing costs remain elevated

- Asset valuations are still sensitive to interest rates

- Market volatility can be amplified by relatively small data surprises

As a result, liquidity management and timing become core pillars of financial planning.

In practical terms:

- A portion of assets should remain readily accessible

- Investors should avoid being forced to sell long-term assets at unfavorable times

- Capital deployment should be gradual and staged, not all at once

Government Debt and Structural Uncertainty

One defining feature of the current cycle is the high level of government debt, particularly in the United States. Even if policy rates decline, heavy bond issuance can keep long-term yields elevated.

For investors, this implies:

- Bond markets may remain volatile

- Risk assets may face ongoing valuation pressure

- Financial planning must balance return objectives with long-term stability

Balancing return and stability means:

- Not allocating all capital toward high-return, high-risk assets

- Maintaining a portion of the portfolio that is lower-volatility, income-oriented, and reliable

- Ensuring the overall financial plan remains resilient even under weaker scenarios

Section Summary: Financial Planning in the 2026 Environment

The outlook for 2026 highlights several realities:

- Economic growth is limited but positive

- Inflation is lower, yet still influential

- Interest rates remain a constraining factor

- Risks are increasingly structural and cumulative

In this context, successful financial planning for 2026 requires:

- Informed and disciplined decision-making

- A strong focus on asset quality

- And a balanced portfolio that supports both present needs and long-term family security

In the next section, we move from analysis to action, outlining practical financial planning steps to prepare effectively for 2026.

Key Financial Planning Tips to Prepare for 2026

A Practical Financial Planning Guide for Families Living in Dubai

At Dar al-Tharwat, our approach to financial planning is grounded in one core belief:

financial analysis only becomes valuable when it translates into clear, practical decisions that families can actually implement in their daily lives.

This is especially important in Dubai.

Dubai is a truly international city. A large portion of its population consists of expatriate families who have recently relocated, often with new careers, new income structures, and a new cost of living. Many of these families are navigating critical questions:

- How should we plan our finances in a new country?

- How do global economic risks affect our financial future in Dubai?

- How can we use Dubai’s access to global markets to our advantage?

In financial planning for 2026, these questions become even more important. Global economic uncertainty, geopolitical risks, and changing monetary policies all influence financial outcomes. At the same time, Dubai offers access to international opportunities that if used wisely can strengthen long-term financial security.

In this section, we aim to make your financial path clearer and more structured, helping Dubai-based families design a financial plan that reflects both global realities and local living conditions.

Start Financial Planning with Dubai’s Lifestyle Reality

The first step in effective financial planning for families in Dubai is understanding the true cost and structure of daily life. Many people begin by asking where to invest, but the more important question is:

“What does our lifestyle in Dubai realistically require?”

Key cost areas include:

- Housing and rent

- International school tuition

- Health insurance

- Transportation and daily living expenses

If these foundations are not properly covered, even strong investment returns will not create real financial security.

Good financial planning in Dubai means:

stabilize daily life first, then pursue growth.

Align Time Horizons with Expat Life Realities

Many families living in Dubai:

- Do not hold permanent residency

- Or anticipate relocating in the future

For this reason, financial planning 2026 must clearly separate assets by time horizon:

- Short-term (0–2 years):

Living expenses, rent, education, insurance - Mid-term (3–7 years):

Savings, balanced investments, potential relocation - Long-term (10+ years):

Retirement, children’s university education, wealth accumulation

Funds that may be needed for relocation or major transitions should not be locked into illiquid assets.

Think Globally When Diversifying Your Portfolio

One of Dubai’s major advantages is access to global financial markets. In portfolio diversification 2026, concentrating wealth in a single country or asset class introduces unnecessary risk.

For Dubai-based families:

- Geographic diversification is essential, not optional

- Exposure across currencies, regions, and asset classes improves resilience

A well-structured financial plan typically includes:

- International assets

- Regional opportunities

- Global long-term holdings

This approach helps protect against localized shocks and policy changes.

Liquidity Is a Financial Safety Shield in Dubai

Dubai’s professional environment is dynamic:

- Employment contracts can change

- Income streams may fluctuate

- Living costs are relatively high

In financial planning for 2026, liquidity plays a critical role.

Practical guidance:

- Maintain coverage for 6–12 months of essential expenses

- Ensure funds are accessible without penalties

At the same time, excessive idle cash without purpose exposes families to inflation risk.

The goal is balance: prepared, but not stagnant.

View Real Estate in Dubai with Realistic Expectations

Real estate is attractive in Dubai, but it should be approached carefully within a broader financial plan.

Before purchasing property, consider:

- Does the asset generate reliable income?

- Are financing costs manageable under higher interest rates?

- How liquid is the property if circumstances change?

In financial planning 2026, real estate should be one component of the portfolio, not the sole pillar of family wealth.

Review and Control Debt Exposure

With interest rates remaining elevated, unmanaged debt can erode financial stability.

Sound financial planning requires:

- Full transparency on borrowing costs

- Comparing investment returns to debt expenses

- Avoiding obligations that reduce savings capacity

If monthly repayments prevent consistent saving or investing, the debt is likely undermining long-term financial goals.

Make Investment Decisions Gradually, Not All at Once

Markets in 2026 are:

- Data-driven

- Highly sensitive

- Prone to short-term volatility

For Dubai-based families with international exposure, phased investment decisions reduce timing risk and increase flexibility.

This principle is a cornerstone of a disciplined investment strategy 2026.

Treat Risk Management as a Core Planning Element

High incomes can sometimes create a false sense of security. In reality, risk management strategies are essential to sustainable financial planning.

For families in Dubai, this includes:

- Adequate health and life insurance

- Defensive assets within the portfolio

- Avoiding reliance on a single income source

A financial plan without risk management is vulnerable to unexpected shocks.

Keep Your Financial Plan Dynamic and Reviewable

Financial planning is not a static document especially in a city like Dubai where personal and professional conditions can evolve rapidly.

As part of long-term financial planning:

- Review your plan at least every six months

- Reassess goals, liquidity, and risk exposure

Adjust decisions based on changing circumstances

Section Summary

For families living in Dubai, financial planning for 2026 is about:

- Aligning financial decisions with real living costs

- Maintaining global diversification

- Managing liquidity, debt, and risk

- Making informed, gradual investment choices

This approach supports:

- Lifestyle stability

- Reduced emotional decision-making

- Greater confidence in navigating global uncertainty

In the next section, we will examine the pros and cons of the financial environment in 2026, helping you weigh opportunities and constraints side by side to refine your financial strategy further.

Pros and Cons of the Financial Environment in 2026

Why Greater Risk Transparency Can Improve Financial Planning

After several highly volatile years, the financial environment of 2026 has entered a different phase. This is not a year of speculative booms, nor a year of broad economic contraction. Instead, it is a year in which risks have become more visible and that visibility, if understood correctly, can actually work in favor of sound financial planning.

For families and investors especially those living in Dubai understanding both the advantages and limitations of this environment helps:

- Reduce emotional decision-making

- Set realistic expectations

- Shift financial planning from reactive to structured and intentional

Below, we examine the key advantages first, followed by the constraints of the 2026 financial landscape.

Advantages of the Financial Environment in 2026

1. Risks Are No Longer Hidden From Invisible Threats to Decision Inputs

One of the most important differences between 2026 and previous years is the visibility of risks.

In earlier periods particularly 2021 and 2022 many risks were largely hidden:

- Interest rates were low, but the speed and magnitude of future hikes were underestimated

- Inflation pressures were not fully recognized early on

- Asset valuations assumed optimistic, low-risk scenarios

What happened as a result?

- Borrowing costs rose abruptly

- High-risk assets experienced sharp corrections

- Many families and investors were caught off guard

In 2026, the situation is different:

- We know interest rates are structurally higher

- We know inflation has not fully disappeared

- We know economic growth is constrained

Why does this matter for financial planning?

Visible risks can be managed. When risks are known, families and investors can:

- Build scenarios

- Adjust portfolio construction

- Make more conservative and informed decisions

This transparency is a meaningful advantage for disciplined financial planning in 2026.

2. Cash-Flow–Generating Assets Gain Importance

In the current environment, price appreciation alone is no longer sufficient. Assets that generate real, recurring cash flow have become increasingly valuable.

Practical examples include:

- Profitable dividend-paying companies

- Income-producing real estate with stable rental demand

- Infrastructure and energy assets linked to essential consumption

In contrast to years when rising prices alone could deliver returns, 2026 places greater emphasis on financial sustainability.

Financial planning insight:

Assets that “produce income” reduce reliance on market timing and help stabilize household finances during periods of volatility.

3. The End of the Illusion That Markets Always Recover Quickly

A subtle but important benefit of the 2026 environment is the disappearance of the belief that markets will always recover immediately.

In previous years:

- Market pullbacks were often short-lived

- This reinforced excessive risk-taking

In the current cycle:

- That assumption no longer holds

- Investors are forced to reassess risk more carefully

Positive outcome:

Financial planning has become more realistic, and speculative behavior has declined.

4. Opportunities for Patient, Long-Term Investors

Although rapid growth is unlikely, 2026 offers opportunities for investors with:

- Long-term horizons

- A focus on portfolio resilience rather than short-term gains

Why?

- Asset prices in many markets are more reasonable

- Valuations better reflect underlying fundamentals

This environment is better suited to long-term financial planning than the speculative years that preceded it.

5. Dubai’s Strategic Advantage in Risk Management and Opportunity Access

For families living in Dubai, one major advantage stands out: financial and geographic flexibility.

Compared with many other regions:

- Access to global markets is broader

- Currency diversification is easier

- Financial infrastructure is internationally connected

This allows Dubai-based families to:

- Spread risk across regions

- Hold assets in multiple currencies

- Adjust portfolios more efficiently as conditions change

This flexibility is a key advantage for portfolio diversification in 2026.

.webp)

Limitations and Risks of the Financial Environment in 2026

1. Economic Growth Is Limited and Fragile

One of the main constraints of 2026 is that growth exists, but it is neither broad nor robust.

This means:

- Market-wide gains are unlikely

- Poor investment choices are penalized more quickly

Financial planning implication:

The era of indiscriminate investing is over.

2. Inflation Is Lower, but Still Disruptive

While headline inflation has declined, certain costs such as:

- Housing

- Education

- Healthcare

continue to rise.

For families, especially in high-cost cities like Dubai, this creates ongoing pressure on purchasing power.

Planning challenge:

Ignoring real (inflation-adjusted) returns can gradually erode financial stability.

3. Interest Rates Remain a Structural Constraint

Even if policy rates decline modestly:

- Financing costs remain elevated

- Leverage becomes riskier

- Asset valuations stay sensitive

Practical takeaway:

In 2026, debt must be carefully managed and strategically justified.

4. Short-Term Volatility Driven by Data and Headlines

Markets in 2026 react quickly to:

- Economic data

- Policy signals

- Geopolitical developments

This can lead to sharp but temporary fluctuations.

Primary risk:

Emotional and rushed decisions not the volatility itself.

5. Geopolitical and Structural Uncertainty Persists

Some risks cannot be forecast precisely, including:

- Geopolitical tensions

- Fiscal pressures from high government debt

- Structural changes in global trade and policy

Financial planning response:

Design portfolios that remain functional even under unfavorable scenarios.

Section Summary

The financial environment of 2026 is characterized by:

- Greater risk transparency

- More selective opportunities

- Structural constraints on growth

For families and investors, this environment is not inherently negative. When approached thoughtfully, it becomes a decision-making framework rather than a threat.

Best Assets to Invest in 2026

How to Select the Right Assets in Financial Planning for 2026

In 2026, the key investment question is no longer:

“Which asset will grow the fastest?”

The more relevant question is:

“Which assets are aligned with today’s global risks and can play a sustainable role in long-term financial planning?”

The financial environment of 2026 is selective:

- Broad market growth is unlikely

- Short-term volatility is present

- Asset quality matters more than market participation

In this section, we examine the best assets to invest in 2026, focusing on logic, resilience, and practical application within a disciplined financial planning framework.

High-Quality, Profitable Equities

The Core of an Investment Strategy for 2026

During years of easy money, many stocks rose purely on growth expectations.

In 2026, that approach is no longer sufficient.

Key Characteristics of Suitable Stocks for 2026 (With Examples)

1. Sustainable Profitability

Companies that generate consistent profits even when economic growth is limited.

Example:

Businesses in essential consumer goods, healthcare, and basic services. People continue to buy food, medicine, and everyday necessities regardless of economic cycles.

2. Strong Balance Sheets

Companies with manageable debt levels that are not heavily exposed to high interest rates.

Example:

Two companies with similar revenues:

- Company A has low debt

- Company B carries high-interest liabilities

In 2026, Company B may lose a large portion of its earnings to interest expenses.

4. Reliable Cash Flow

Actual cash generation not just accounting profits.

Example:

A healthcare services company with regular payments

versus a project-based firm with irregular cash inflows.

Financial planning insight:

Stocks that generate real cash flows provide stability in uncertain markets, even if prices fluctuate.

ETFs and Diversified Funds

Smart Tools for Portfolio Diversification in 2026

For many families especially expatriates living in Dubai managing global markets directly can be complex.

This is where ETFs and diversified funds become valuable.

Why ETFs Matter in 2026

- Automatic diversification

- Lower single-stock risk

- Transparency

- Lower costs compared to active management

Practical example:

Instead of selecting several volatile individual stocks,

a global dividend or developed-market ETF can reduce portfolio risk.

Role in financial planning:

ETFs are effective tools for mid- to long-term capital allocation and portfolio diversification 2026.

Real Estate: Focus on Cash Flow, Not Price Appreciation

Real estate particularly in Dubai remains attractive, but the logic has changed.

In financial planning for 2026:

- Good real estate = income-generating real estate

- Not property purchased solely for price appreciation

Key Criteria for Real Estate in 2026

- Stable rental income

- Reasonable price-to-rent ratios

- Predictable maintenance costs

- Acceptable liquidity if circumstances change

Financial planning takeaway:

Real estate should be one component of a diversified portfolio, not the entire strategy.

Gold and Precious Metals

Value Preservation, Not a Growth Engine

The strong performance of gold in recent years highlighted its role as a defensive asset.

In 2026:

- Gold is primarily a risk-management tool

- Not a vehicle for aggressive growth

Practical example:

During geopolitical tensions or financial shocks, gold can help offset declines in other assets.

Role in Financial Planning 2026:

Portfolio balance and downside protection.

Real Assets: Energy, Infrastructure, and Select Commodities

Real assets gain importance in environments where inflation has not fully disappeared.

Why Real Assets Matter

- Revenues linked to real economic consumption

- Often move in line with inflation

- Enhance portfolio resilience

Examples:

- Energy assets

- Infrastructure investments

- Selected industrial commodities

Role in long-term financial planning:

Preserving purchasing power rather than chasing short-term gains.

Liquidity: An Invisible but Essential Asset

Liquidity itself does not generate growth, but in 2026 it plays a critical role.

Key balance:

- Too little liquidity → forced asset sales during downturns

- Too much liquidity → erosion of value through inflation

Financial planning principle:

Liquidity provides flexibility not long-term wealth storage.

Assets That Require Greater Caution in 2026

Certain assets warrant increased caution:

- Highly speculative investments

- Assets without cash flow

- Projects with long promises but limited transparency

Key insight:

In 2026, saying “no” to some opportunities is part of sound financial planning.

Section Summary

The best assets to invest in 2026 are not necessarily:

- The most exciting

- Or the fastest-growing

Effective financial planning 2026 focuses on:

- Asset quality

- Reliable cash flows

- Intelligent diversification

- Balance between growth and stability

In the next section, we turn to one of the most critical pillars of financial decision-making:

Risk Management Strategies for 2026

How to Protect Your Capital and Family’s Financial Future in Financial Planning 2026

In 2026, risk is no longer abstract or theoretical.

Risks are visible, measurable, and impactful, which makes risk management one of the central pillars of financial planning for 2026.

The objective of risk management is not to eliminate risk entirely.

Rather, it is to control, distribute, and keep risk within tolerable limits especially for families and long-term investors.

In this section, we outline the most important risk management strategies that families particularly those living in Dubai can apply in practice.

True Diversification: The First Line of Defense

One of the most common misconceptions is:

“I own several assets, so my portfolio is diversified.”

True diversification means:

- Diversification across asset classes

- Diversification across income sources

- Diversification across geographies and currencies

Practical example:

If all your assets depend on:

- One market

- One currency

- One economic policy

you still carry concentration risk even if you hold multiple instruments.

In portfolio diversification 2026, combining:

- Equities

- Real estate

- Real assets

- Gold

- Liquidity

across different regions significantly reduces overall portfolio risk.

Liquidity Management: Avoiding Forced Decisions

One of the most dangerous risks in financial planning is forced liquidation risk having to sell long-term assets at the wrong time.

Practical example:

A family without sufficient liquidity who suddenly faces:

- Medical expenses

- Job disruption

- Relocation costs

may be forced to sell property or long-term investments at unfavorable prices.

Actionable guidance for financial planning 2026:

- Maintain 6–12 months of essential living expenses in liquid or near-liquid assets

Treat liquidity as a risk management tool, not idle cash.

Separate Capital by Time Horizon

A core principle of effective risk management is:

Never expose short-term needs to long-term volatility.

In long-term financial planning, capital should be clearly segmented:

- Short-term capital: low risk, high liquidity

- Mid-term capital: balanced risk and return

- Long-term capital: growth-oriented with volatility tolerance

Example:

Funds intended for:

- School tuition

- Rent

- Potential relocation

should not be invested in highly volatile assets even if expected returns are higher.

Debt Risk Control in a High-Interest-Rate Environment

In 2026, debt represents one of the most significant sources of financial risk.

Higher interest rates mean:

- Larger repayment burdens

- Increased cash-flow pressure

- Reduced financial flexibility

Debt risk management means:

- Full transparency on borrowing terms

- Comparing debt costs with realistic investment returns

- Avoiding leverage that dominates the financial plan

Key insight:

If debt repayments eliminate your ability to save or invest, that debt is a risk not a tool.

Using Defensive Assets to Balance the Portfolio

Not all assets in financial planning 2026 are chosen for growth.

Some assets exist to absorb shocks.

Common defensive assets include:

- Gold and precious metals

- Certain real assets

- Low-volatility income-generating investments

Practical role:

When equity markets correct, these assets can help limit overall portfolio drawdowns.

Personal and Family Risk Management (Beyond Markets)

Risk management is not limited to investments.

For families especially expatriates living in Dubai personal risks are equally critical.

Key risks include:

- Health risk

- Disability or loss of income

- Family dependency risk

Essential tools:

- Adequate health insurance

- Life insurance

- Contingency income planning

Important reminder:

A strong investment portfolio without personal risk coverage is incomplete.

Phased Decision-Making to Reduce Timing Risk

Markets in 2026 are data-driven and sensitive to headlines.

Large, one-time investment decisions increase timing risk.

Effective risk management strategy:

- Deploy capital in stages

- Maintain flexibility to adjust decisions as conditions evolve

This approach is a cornerstone of a disciplined investment strategy for 2026.

Regular Review and Adjustment of the Financial Plan

Risk profiles do not remain static.

In financial planning 2026, effective risk management requires:

- Ongoing monitoring

- Periodic adjustment

- Rational not emotional responses to change

Actionable recommendation:

Review your financial plan at least every six months, reassessing:

- Asset allocation

- Liquidity levels

- Debt exposure

- Risk tolerance

Section Summary

In financial planning for 2026, risk management is:

- Not optional

- Not secondary

- But a central decision-making framework

Successful risk management helps families:

- Avoid forced financial decisions

- Preserve flexibility

- Build financial plans that remain functional even in adverse scenarios

In the next section, we will focus on Important Financial Charts to Watch in 2026, highlighting the indicators that help investors and families make timely, informed decisions.

Risk Management Checklist for Financial Planning 2026

A Practical Checklist for Families and Long-Term Investors

Use this checklist to evaluate whether your financial planning for 2026 is properly protected against key risks.

1. Portfolio Diversification (Portfolio Diversification 2026)

☐ Are my assets diversified across multiple asset classes (equities, real estate, real assets, gold, cash)?

☐ Do I have exposure to different geographic regions (not just one country)?

☐ Is my portfolio diversified across more than one currency?

☐ Am I overly dependent on a single market, sector, or investment theme?

2. Liquidity Management

☐ Do I have 6–12 months of essential living expenses available in liquid or near-liquid assets?

☐ Can I access emergency funds without penalties or forced selling?

☐ Is my liquidity level planned, not accidental?

☐ Am I avoiding excessive idle cash that loses value to inflation?

3. Time Horizon Alignment (Long-Term Financial Planning)

☐ Are short-term needs separated from long-term investments?

☐ Is capital needed within the next 1–3 years protected from high volatility?

☐ Are long-term investments allowed to tolerate short-term market fluctuations?

☐ Do I clearly understand the purpose of each investment?

4. Debt Risk Control

☐ Do I fully understand the interest rates and repayment terms of all debts?

☐ Are my debt repayments sustainable under higher interest rates?

☐ Can I continue saving and investing while servicing my debt?

☐ Is my debt supporting long-term goals or limiting financial flexibility?

5. Defensive Assets Allocation

☐ Does my portfolio include defensive or shock-absorbing assets (e.g. gold, low-volatility income assets)?

☐ Am I relying solely on growth assets for returns?

☐ Can my portfolio withstand short-term market corrections without panic selling?

6. Personal & Family Risk Coverage

☐ Do I have adequate health insurance coverage?

☐ Is there life insurance or income protection for dependents?

☐ Have I considered risks related to employment, relocation, or health disruptions?

☐ Is my financial plan resilient to non-market risks?

7. Decision Timing & Investment Strategy 2026

☐ Do I invest capital gradually, rather than all at once?

☐ Am I avoiding emotionally driven investment decisions?

☐ Is my investment strategy flexible enough to adapt to new data?

☐ Do I regularly reassess assumptions behind my decisions?

8. Ongoing Review & Adjustment

☐ Do I review my financial plan at least every six months?

☐ Is my asset allocation still aligned with my goals and risk tolerance?

☐ Have I adjusted my plan for changes in income, family needs, or market conditions?

☐ Is my financial planning proactive rather than reactive?

Final Reminder

✔️ Risk management in financial planning 2026 is not about avoiding uncertainty.

✔️ It is about being prepared, maintaining flexibility, and protecting long-term stability.

A financial plan that passes this checklist is far more likely to remain effective even when markets, policies, or personal circumstances change.

Important Financial Charts to Watch in 2026

A Simple Guide for Families to Make Better Financial Decisions

In 2026, successful financial planning is not only about choosing the right assets.

It is also about understanding what is happening around you without stress, panic, or over-analysis.

These charts are not for traders and not for daily monitoring.

They are tools to help families answer one simple question:

Should we be more careful right now, or can we move a bit more confidently?

Below are the only charts families really need for financial planning in 2026 explained in plain language.

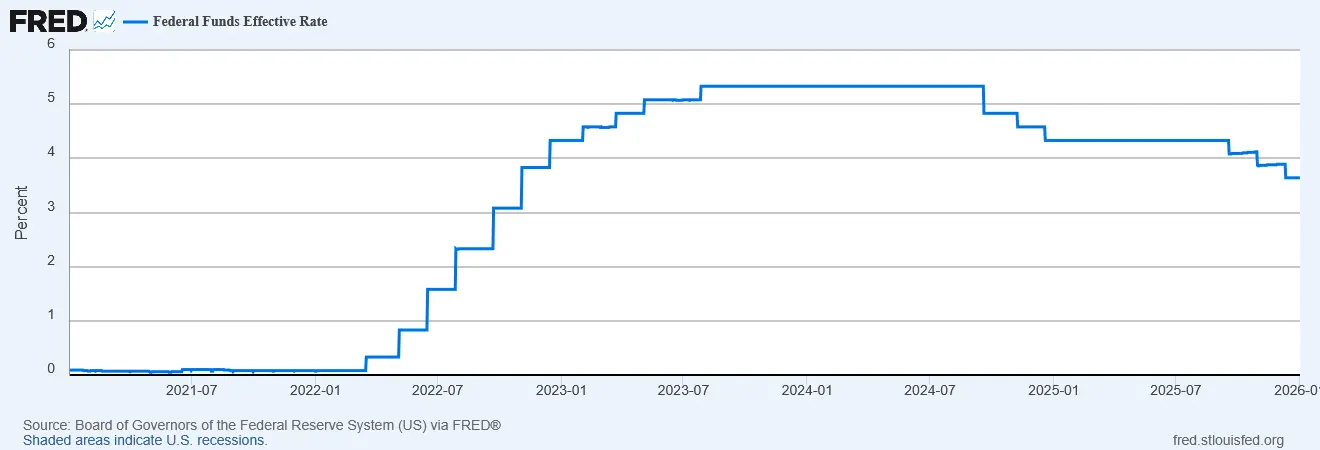

1. Interest Rate Chart

Is Money Expensive or Getting Cheaper?

What interest rates mean (in simple terms)

Interest rates tell you:

- How expensive borrowing is

- How difficult it is for businesses and families to grow using debt

Real-life example:

When interest rates are high:

- Loan payments increase

- Mortgages feel heavier

- Families spend more carefully

When rates go down:

- Pressure slowly eases

- Investment and spending become easier

What 2026 looks like

- The big interest-rate shock is over

- But rates are still high compared to the past decade

What this means for families

- Be careful with new loans

- Avoid heavy debt

Keep enough cash flexibility.

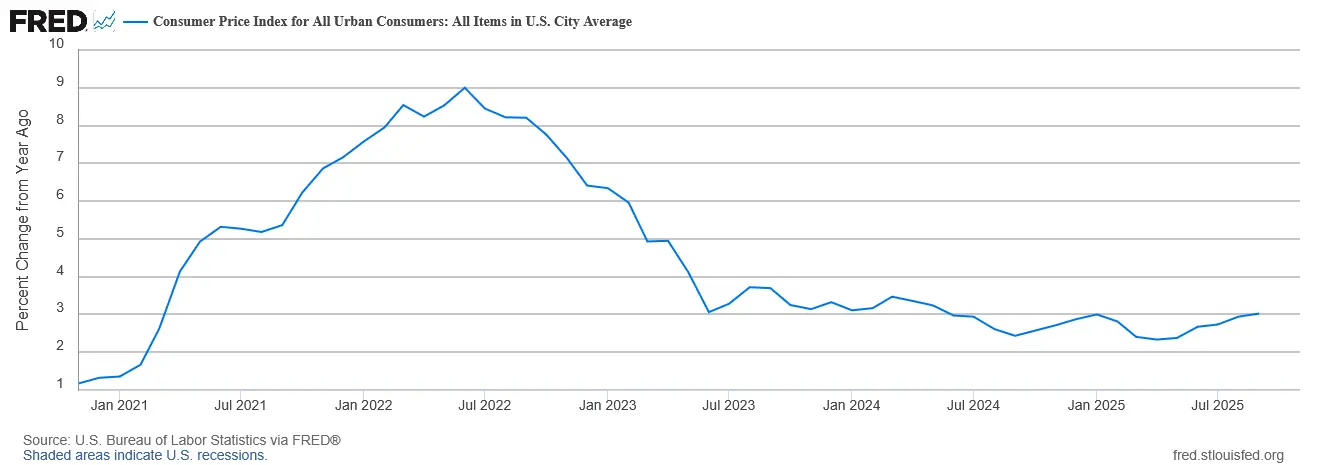

2. Inflation Chart

Why Inflation Still Matters (Even If It Is Lower)

What inflation really means

Inflation means:

Your money buys less than it used to.

Everyday example:

Costs such as:

- Rent

- School fees

- Healthcare

- Insurance

rarely go down quickly.

The key issue in 2026

Overall inflation has declined,

but service inflation remains sticky.

What this means for financial planning

- Looking only at investment returns is misleading

- You must ask:

“Am I gaining after inflation, or just keeping up?”

Simple example:

- Investment return: 7%

- Inflation: 5%

- Real gain: only 2%

3. Yield Curve Chart

Is the Market Confident or Worried About the Future?

The name sounds complicated, but the idea is simple.

What the yield curve tells us

It shows whether investors feel:

- Confident about the future

- Or worried and cautious

Simple logic:

- When people worry about the future → short-term rates stay high

- When confidence improves → long-term rates rise normally

Why families should care

This chart helps answer:

“Should we slow down and be cautious, or can we gradually take more risk?”

.webp)

4. Stock Market Index Chart

Are Markets Calm or Over-Excited?

Stock market indexes do not tell us when to buy or sell.

They help us understand market mood.

What indexes show

- Fear vs confidence

- Calm growth vs emotional rallies

Simple example:

- Very fast price increases → higher correction risk

- Slow, steady movement → healthier environment

How families should use this

Not to trade but to adjust risk exposure:

“Do we increase risk slowly, or stay conservative?”

6. Government Bond Market Chart

The Market’s “Fear Gauge”

Bond markets act like a thermometer.

Simple idea:

- When investors are afraid → they buy safe bonds

- When confident → they move toward risk assets

What families should understand

- High bond market volatility = caution

Calm bond markets = stability

.webp)

7. Liquidity Conditions

Is Money Flowing Easily or Not?

Liquidity means:

- How easy it is to access money in the system

2026 reality

- Liquidity is tighter

- Money is more selective

Practical takeaway

- Avoid investing all funds at once

- Use step-by-step decisions

Keep flexibility

How to Use These Charts (Without Stress)

These charts are not for daily checking.

Correct use:

- Monthly or quarterly review

- To adjust direction not react emotionally

The right question is:

“Should we be more cautious or slightly more active?”

Not:

“Should we buy or sell today?”

Simple Summary of Section 6

In financial planning for 2026:

- Understanding the environment matters more than predicting it

- Calm, informed decisions outperform emotional reactions

Charts are not there to scare you. They are there to bring clarity and confidence.

Plan Your Financial Strategy for 2026

If you're living in Dubai and want a structured financial plan built around your income, goals, and global investment opportunities, our advisors can help you design a strategy tailored to your situation.

Speak with a Financial Consultant